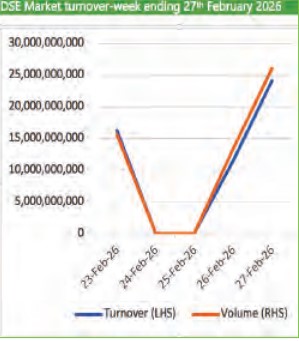

DSE weekly activities decline

DAR ES SALAAM: THE Dar es Salaam Stock Exchange (DSE) recorded a drop in activities during the week, with a lower turnover compared to the previous week. Equity turnover amounted to 51.7bn/-. On a weekon-week basis, total market turnover decreased by 41 per cent, falling from 87.8bn/- recorded in the prior week.

Trading activity was largely driven by CRDB, which accounted for 56.67 per cent of total market turnover. NMB followed with a 17.31 per cent contribution, while TCC and KCB represented 11.26 per cent and 8.6 per cent of total turnover, respectively.

On the price performance front, Banks continue to dominate gains during the week, MCB leading with a sharp increase to reach 1,900/- per share equal to a 33.8 per cent increase, DCB recorded a 23.96 per cent increase in price to reach 595/- price per share, MBP and TOL reported gains as well reporting 14.4 per cent and 12.92 per cent gains respectively closing the week at 2,860/- and 1,005/-.

Conversely, on the losers side NMG was the week’s top laggard, shedding 6.67 per cent to close at 280/- per share. DSE declined by 1.9 per cent to 6,720/- while TCCL fell by 1.88 per cent to close at 3,140/-. TBL also recorded a notable decline of 1.36 per cent, ending the week at 10,130/- per share.

SWIS ended the week at 2,690/- per share equal to a drop of 0.74 per cent. From a valuation perspective, the exchange recorded gains in both total and domestic market capitalisation.

Total market capitalisation edged up 2.63 per cent to 34.6tri/-, while domestic market capitalisation increased by 2.23 per cent to close the week at 24.25tri/-.

Focus shifts to upgrade path after Moody’s affirmed Tanzania rating Tanzania’s reaffirmation at B1 by Moody’s Ratings has eased immediate concerns of a down-grade, but attention is increasingly turning to what the country must do to secure a higher credit rating.

The agency maintained a stable outlook, projecting real gross domestic product (GDP) growth of at least six percent in the in medium term, supported by investment in manufacturing, mining, tourism and transport. Inflation closed 2024 at 3.1 per cent, while the fiscal deficit stood at three per cent of GDP.

ALSO READ: NEVER AGAIN: Youth urged to guard Tanzania’s peace

The decision signals continued confidence in Tanzania’s macroeconomic framework despite political tensions surrounding the 2025 General Election. However, analysts caution that the B1 rating still within speculative grade underscores that stability alone will not significantly reduce borrowing costs or unlock access to cheaper long-term capital. Current account deficit narrows 28.7 per cent since November.

The current account deficit narrowed to 1.91 billion US dollars in the period ending November last year from 2.68 billion US dollars a year earlier, buoyed by strong goods and services exports that improved the external balance. The latest Bank of Tanzania Monthly Economic Review shows that there was also a moderate increase in imports, largely reflecting higher demand for inputs used in production and investment activities.

This pattern suggests an expansion in domestic economic activity, as firms increase imports of intermediate goods and capital equipment to support manufacturing, construction and infrastructure projects. Such import growth is indicative of improving investment conditions and business confidence, rather than consumption-driven demand from an economic standpoint, the rise in production and investment-related in ports is expected to strengthen productive capacity and enhance output in the medium to long term.

Treasury bill auction no: 1193 On February 25, 2026, Central Bank was in the market offering treasury bills to investors. The offerings included 29.9bn/- for the 35- day maturity Treasury bill, 39.9bn/- for the 91-day T-bill, 59.9bn/- for the 182-day Tbill and 85.2bn/- for the 364- day T-bill. Investor demand in this auction was relatively strong across all maturities, with all Treasury bills recording oversubscription.

The 35-day bill achieved a subscription rate of 367.89 per cent, the 91-day bill 290.1 per cent, the 182-day bill 248.77 per cent and the 364- day bill also attracted solid interest, posting a subscription rate of 145.27 per cent. Despite the strong demand across all maturities, the Bank of Tanzania allotted exactly the amounts offered for each maturity, with the exception of the 364-day bill, where the Bank accepted more than the initially offered amount.

The 364-day Treasury bill recorded a marginal decline in its weighted average yield, easing from 6.2295 per cent in the mid February auction to 6.1683 per cent in the current auction a decrease of 6.12 basis points. This slight drop in yield was supported by an increase in the minimum successful price, which rose to 94.1400 from 94.0005 in the previous auction. Meanwhile, the inflation rate for January 2026 stood at 3.3 per cent.